Alan Livsey in the FT:

Alan Livsey in the FT:

Donald Trump was thinking about the teenage climate activist Greta Thunberg when he took aim at what he called the “prophets of doom” at Davos in January. But just as easily he could have been targeting global investors whose trenchant criticism of hydrocarbons has led to a shift in investment away from the traditional energy sector and into renewables.

This move represents a big problem for energy groups such as Exxon, BP and Saudi Aramco. Vast swaths of their oil, gas and coal reserves may never be extracted and burnt because doing so would intensify global warming, worsening freak weather events and threatening the loss of farmland and huge population displacement. That could leave them with large numbers of what are known as “stranded assets”.

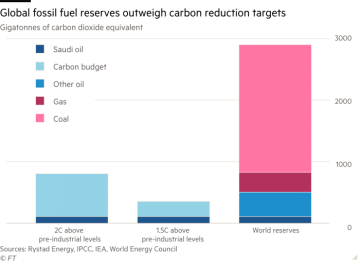

In that context of the climate emergency, the cost of writing off stranded assets could be seen as a small price to pay. But the amounts involved would be breathtaking. According to Lex estimates, around $900bn — or one-third of the current value of big oil and gas companies — would evaporate if governments more aggressively attempted to restrict the rise in temperatures to 1.5C above pre-industrial levels for the rest of this century.

Even in what the industry might see as the more benign case of a 2C rise — which was the target countries agreed to meet at the 2015 Paris Agreement on climate change — energy producers, including coal miners, would have to write off over half of their fossil fuel reserves as stranded. If the 1.5C threshold were to be met then the pain would be greater, leaving over 80 per cent of hydrocarbon assets worthless.

More here.