William Janeway over at INET:

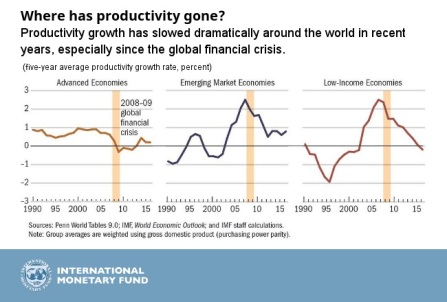

Productivity is the key driver of economic growth. It is the force that increases output of goods and services beyond what increased inputs of labor, capital and other factors of production like energy can account for. So growth in productivity increases income per head, the size of the pie available for distribution. And, as conventionally defined, the “Productivity Puzzle” is the unexplained decline in the growth of productivity observable over the past decade, through the recovery from the Great Recession triggered by the Global Financial Crisis of 2008. Here is the IMF’s picture for the advanced economies:

https://blog-imfdirect.imf.org/2017/03/13/chart-of-the-week-the-productivity-puzzle/

In fact, the decline in productivity growth has a longer history: over the past 30 years, with the exception of the uptick during the years of the great Dotcom/Internet Bubble of the late 1990s, productivity growth has slowed markedly.

Gavyn Davis, “Is Economic Growth Permanently Lower?” available at https://www.ft.com/content/3822867f-85bf-33a2-85a5-4a40974d7d9e

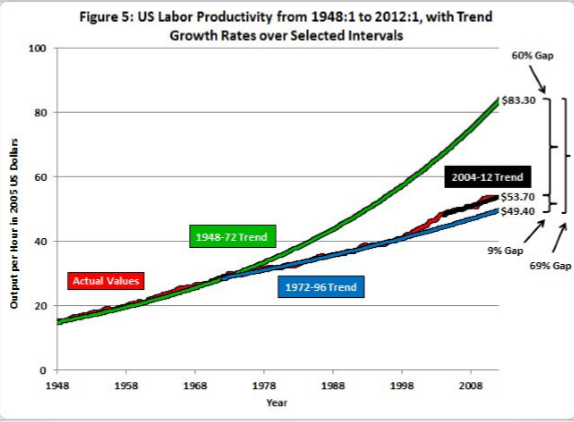

Post-war reconstruction, especially of the devastated economies of western Europe and Japan, was responsible for a rate of growth in productivity that was unsustainable. But in 2012, ignoring the one-off character of the 15 years to 1972 and focusing on the US, the distinguished economic historian Robert Gordon established himself as a leading techno-skepticist. In his provocative essay “Is U.S. Economic Growth Over?” Gordon graphically dramatized the divergence from the previous trend that began in 1972:

One mode of response to Gordon and to the data has been to focus on the potential mismeasurement of output in the increasingly digalized economy, since any such shortfall would automatically reduce the measured rate of growth in productivity. Thus, MIT’s Erik Brynjolfsson and Joohee Oh, note:

Over the past decade, there has been an explosion of digital services on the Internet, from Google and Wikipedia to Facebook and YouTube. However, the value of these innovations is difficult to quantify, because consumers pay nothing to use them.

But their estimate of the missing output is only $30 billion, barely a rounding error in a $18 trillion economy.

Recently, leading economist of innovation Philippe Aghion and colleagues have identified what appears to be a substantially larger source of under-measurement of productivity in the over-statement of inflation.

More here.